Zepto should not be audited as a simple FY25 loss story. That would be lazy, and it would miss the harder capital-market question now forming around the company. The more serious story is that Zepto is entering the IPO corridor with two competing truths on the table: a brutal FY25 base that shows the cost of buying speed, and an FY26 repair claim that says the burn curve is finally bending before public-market scrutiny arrives.

The first truth is numerical and uncomfortable. Zepto’s FY25 total income reportedly rose 129% to ₹9,668.8 crore, but net loss widened 177% to ₹3,367.3 crore. The second truth is more provisional: before the IPO, Zepto is reportedly telling investors that cash burn has materially reduced, dark-store expansion has slowed, order volumes have risen without major network addition, and full-year profitability is being targeted by FY29. These two truths do not cancel each other. They create the actual Projection Gap.

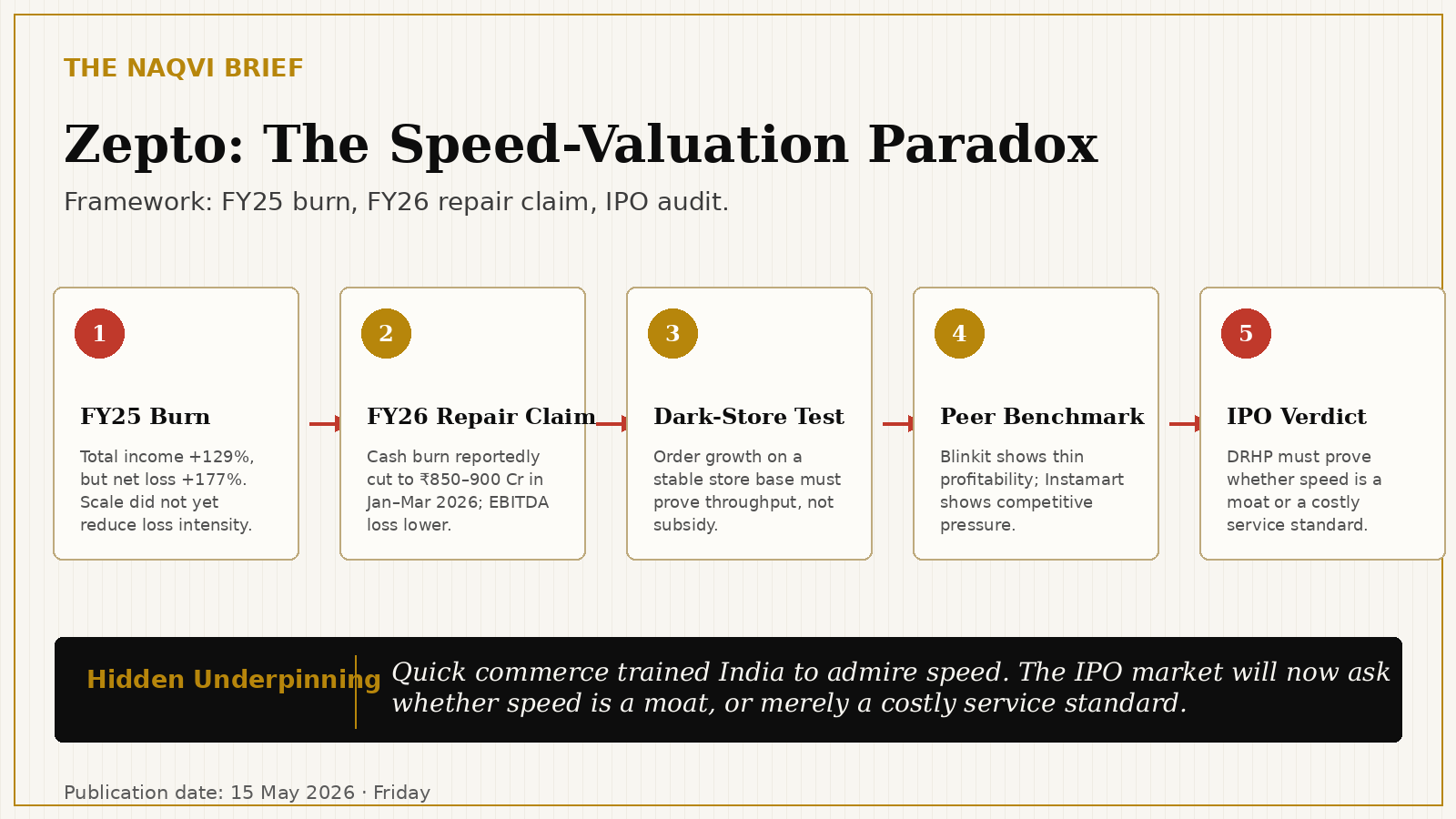

The Correct Frame: FY25 Burn, FY26 Repair Claim

Zepto’s full audited FY26 financials are not yet publicly available, and that matters. The responsible forensic method is not to pretend that FY26 has been fully disclosed. The correct method is to treat FY25 as the hard financial base and FY26 as the pre-IPO operating claim that must be verified when the updated DRHP is filed. This distinction is important because IPO narratives are often repaired first in investor conversations and only later tested in statutory disclosure.

Zepto has reportedly received SEBI approval for its IPO and is expected to file an updated DRHP within six to eight weeks, with the issue size now discussed around ₹8,000–9,000 crore in recent reporting. That means the public-market audit is imminent, but not complete. The central question is no longer whether Zepto can grow. It clearly can. The question is whether growth is becoming economically cleaner fast enough to deserve public-market capital before quick commerce enters a harsher profitability cycle.

The Financial Autopsy: The FY25 Base

| Metric | FY24 | FY25 | Change | Forensic Reading |

|---|---|---|---|---|

| Total income | ₹4,223.9 Cr | ₹9,668.8 Cr | +129% | Demand capture is real |

| Net loss | ₹1,214.7 Cr | ₹3,367.3 Cr | +177% | Losses expanded faster than income |

| Loss as % of total income | 28.8% | 34.8% | Deterioration | Scale did not reduce loss intensity |

| Income per ₹1 of loss | ₹3.48 | ₹2.87 | Decline | Loss efficiency weakened |

| Incremental income | NA | ₹5,444.9 Cr | Large addition | Growth was powerful |

| Incremental loss | NA | ₹2,152.6 Cr | Very large addition | Growth remained expensive |

| Incremental loss / incremental income | NA | 39.5% | Severe | Every ₹100 of new income carried ₹39.5 of new loss |

The FY25 table does not say Zepto is failing. It says something more precise: Zepto proved demand before it proved profit quality. This matters because public markets do not reward scale the same way private markets do. Private capital can finance speed as an option on future dominance. Public capital eventually asks whether the dominance, once achieved, produces cash.

The most damaging FY25 number is not the ₹3,367.3 crore loss by itself. It is the relationship between growth and loss. Total income rose sharply, but loss intensity worsened from 28.8% to 34.8% of income. That means scale did not yet show operating leverage in the reported base year. For a company preparing to sell the quick-commerce dream to public investors, that is the first crack in the valuation story.

The FY26 Counterclaim: Repair or IPO Dressing?

The FY26 counterclaim is serious and should not be dismissed. ET reported that Zepto reduced quarterly cash burn to ₹850–900 crore in the January–March 2026 period from roughly ₹1,200–1,300 crore a few quarters earlier. The same reporting said the improvement was driven by lower per-order costs and a pullback in network expansion, with dark-store count holding at around 1,100. ET also reported that Zepto’s EBITDA loss in the March 2026 quarter was around ₹55–60 crore, down from roughly ₹100–110 crore in the July–September period.

If these claims are true and sustainable, they suggest that Zepto may be entering the IPO with a better operating story than its FY25 numbers alone imply. The company is reportedly pitching breakeven in FY28 and full-year profitability by FY29. The story being sold is not “we are burning forever”; it is “the burn curve is bending”. The forensic problem is that investors must distinguish durable unit-economic repair from temporary pre-IPO cost discipline.

The Dark-Store Test

Quick commerce is not software. It is urban infrastructure. The app is the surface; the machine underneath is dark stores, inventory, riders, demand forecasting, supplier terms, advertising revenue, spoilage control, private labels and neighbourhood density. That is why Zepto’s reported dark-store discipline matters more than the usual startup growth language.

ET reported that Zepto has been pitching growth in order volumes without materially expanding its dark-store network. Its footprint of around 1,100 dark stores has reportedly remained largely unchanged since late last year, while January–March order volumes averaged 2.4–2.5 million orders per day and grew 25–30% sequentially, driven by discounts and free-delivery schemes aimed at order frequency. That sentence contains both the bull case and the warning sign. If Zepto is increasing order volumes on the same store base, throughput economics may be improving. But if that growth is driven heavily by discounts and free delivery, then the model may still be buying frequency rather than monetising loyalty.

The Speed-Valuation Trap

Zepto’s brand proposition is built around speed. That is powerful because it changes behaviour. Once consumers experience rapid fulfilment, planning friction reduces. The city begins to feel like an instant inventory layer, with milk, fruit, snacks, coffee, electronics, beauty products, daily essentials and impulse purchases only minutes away. This is a real behavioural shift, and it explains why quick commerce has become one of India’s most important consumer-internet categories.

But convenience is not the same as pricing power. A customer may love speed and still compare prices, chase discounts, split orders across apps and abandon the platform if fees rise. This is the first trap: the market may mistake frequency for loyalty. The second trap is that speed creates a new cost standard. Once ten-minute delivery becomes expected, every serious player must fund dark-store proximity, inventory depth and rider availability. If the whole sector competes on speed, speed may stop being a premium feature and become a baseline expense.

The Peer Benchmark: Blinkit and Instamart Are No Longer Theoretical Comparisons

Zepto’s IPO will not be judged in isolation. It will be judged against listed peers whose numbers are already public. Blinkit reported adjusted EBITDA of ₹37 crore in Q4 FY26, compared with ₹4 crore in Q3 FY26 and a ₹178 crore loss a year earlier. Blinkit’s net order value grew 95.4% year-on-year to ₹14,386 crore, and it ended the quarter with 2,243 stores. That gives public investors a clear benchmark: quick commerce can show operating profit, but at thin margins and enormous physical scale.

Swiggy’s Instamart provides the other side of the benchmark. Reuters reported that Swiggy’s shares fell after Q4 FY26 results as quick-commerce slowdown and competition clouded a narrower quarterly loss. Analysts focused on Swiggy losing quick-commerce share to Blinkit, while competition from Zepto, Amazon and Flipkart remained intense. The implication for Zepto is sharp: Blinkit is showing that profitability is possible, while Instamart is showing that growth can slow under competitive pressure. Zepto must prove that it can combine the best of both: high growth without returning to severe burn.

The Low-Fee Problem

The quick-commerce consumer has been trained to expect speed, discounts, broad assortment and low friction. That is a beautiful consumer proposition, but a dangerous margin promise. If Zepto wants public-market economics, the burden of funding the service must eventually shift from investors to the operating model. There are only a few possible sources of cash: customers can pay more through fees or larger baskets, brands can pay more through advertising, suppliers can fund economics through terms, private labels can improve gross margins, dark stores can become more productive, and riders can become more efficient through routing and batching.

Each of these helps, but none is automatic. The harder issue is whether these improvements can happen without damaging the behaviour that created growth. If Zepto raises fees too sharply, users may defect. If it cuts discounts too quickly, frequency may weaken. If it squeezes suppliers, supplier support may reduce. If it pushes private labels too aggressively, customer trust may be tested. The path to profitability exists, but it runs through a narrow corridor.

The Unit-Economic Reconstruction

A precise order-level reconstruction must wait for the updated DRHP because investors need verified data on gross order value, order count, average order value, contribution margin, mature-store economics, rider cost, promotional spend, advertising income, private-label mix and inventory losses. Until those numbers are public, the responsible approach is to use reported numbers as proxies rather than false precision.

| Unit-Economic Proxy | FY25 / FY26 Signal | Interpretation |

|---|---|---|

| FY25 total income growth | +129% | Demand capture is real |

| FY25 net loss growth | +177% | Losses scaled faster than income |

| FY25 loss / total income | 34.8% | Material loss intensity |

| FY25 incremental loss / incremental income | 39.5% | New scale still carried heavy burn |

| Jan–Mar 2026 cash burn | ₹850–900 Cr | Lower than earlier ₹1,200–1,300 Cr range |

| Mar 2026 quarter EBITDA loss | ₹55–60 Cr | Better than ₹100–110 Cr in Jul–Sep |

| Dark-store count | Around 1,100 | Network expansion reportedly paused |

| Order volume | 2.4–2.5 million orders/day | Higher throughput claim |

| Growth driver | Discounts and free-delivery schemes | Quality of demand still needs audit |

This table is the real article. FY25 shows the cost of buying scale. FY26 shows the repair claim. The updated DRHP must show whether the repair is durable.

The “Where Does The Cash Come From?” Test

Every quick-commerce company must eventually answer where the cash comes from. Zepto’s IPO story cannot rely on “India loves speed” alone, because demand is no longer the disputed point. The disputed point is whether speed can be monetised at margins that justify a technology valuation rather than a retail-logistics valuation.

| Cash Source | What Must Be True | Risk |

|---|---|---|

| Customer fees | Users value speed enough to pay | Demand may weaken if fees rise |

| Higher AOV | Customers consolidate baskets | Quick commerce often encourages small urgent orders |

| Brand advertising | Brands pay for visibility at purchase point | Works only if traffic quality is strong |

| Private labels | Zepto earns higher gross margin | Requires trust and working-capital discipline |

| Supplier terms | Suppliers fund platform economics | Supplier leverage may resist compression |

| Dark-store productivity | More orders per store without proportional cost | Requires dense and stable local demand |

| IPO proceeds | Balance sheet funds expansion | Capital availability does not prove profit pool |

The highest-quality version of Zepto is not merely a faster delivery company. It is a high-throughput urban retail infrastructure layer with advertising income, private-label margin, efficient inventory turns and dense store utilisation. The low-quality version is a discount-funded delivery engine with beautiful consumer experience and weak cash conversion. The IPO market must decide which version is closer to reality.

The Post-DRHP Audit Checklist

The updated DRHP will determine whether this is a maturing quick-commerce leader or another Projection Gap warning. Investors should not be satisfied with total income, order growth and dark-store count. Those numbers are useful, but they do not prove economic durability. The audit checklist is clear: gross order value, order count, AOV trend, contribution margin by mature versus new dark stores, rider cost per order, promotional spend as a percentage of GOV, advertising income, private-label contribution, inventory losses, working-capital cycle, city-level profitability, cohort retention after fee normalisation and dark-store throughput. Without these disclosures, public investors are being asked to buy speed without seeing whether speed pays for itself.

Status Quo Projection: 3 to 5 Years

| Scenario | Probability | What Happens | Investor Meaning |

|---|---|---|---|

| Best Case | 25% | Zepto improves throughput on the same store base, raises AOV, scales ad revenue and reduces loss intensity sharply | IPO works as growth capital for a maturing quick-commerce leader |

| Base Case | 45% | Revenue and order volumes grow, but discounts, free delivery and competitive pressure keep margins thin | Valuation multiple remains capped despite strong growth |

| Bear Case | 25% | Blinkit widens profitability advantage, Instamart becomes more disciplined, and Zepto must keep burning to defend share | Public markets treat Zepto as a high-growth but expensive challenger |

| Systemic Risk Case | 5% | Quick commerce is repriced as low-margin urban retail infrastructure rather than a technology platform | Sector multiples compress and IPO appetite weakens |

The base case is not failure. The base case is valuation deflation. Zepto may keep growing rapidly and still disappoint investors if the market concludes that quick commerce deserves a logistics-retail multiple rather than a platform-technology multiple.

The Recovery Roadmap

Zepto does not need to abandon aggression. It needs to make the repair claim measurable. The company should use the updated DRHP as a credibility document, not merely an IPO marketing document. First, Zepto should separate mature-store economics from new-store economics. If mature dark stores are contribution-positive or approaching contribution profitability, investors can understand the lifecycle. Second, it must prove that order-volume growth without major dark-store expansion is not merely discount-driven. Throughput improvement is valuable only if it survives incentive normalisation.

Third, the company must show advertising and brand monetisation as a serious margin layer, because quick-commerce shelves are valuable only if brands pay meaningfully for purchase-point visibility. Fourth, Zepto must explain how it can maintain the consumer promise of speed, low fees and attractive pricing while improving margins. A model cannot permanently offer premium service at discount economics unless another revenue pool pays for the gap. Fifth, the company must demonstrate category discipline. Electronics, beauty, café, fashion and daily essentials can raise basket value, but they also add inventory, returns, spoilage, quality and forecasting complexity.

Quick commerce is India’s most elegant example of infrastructure disguised as software. The consumer sees an app. The investor must see a dense physical system of dark stores, riders, inventory, supplier terms, advertisements, private labels and neighbourhood-level demand prediction.

Private markets rewarded the surface because the consumer experience looked magical. Public markets will audit the machine beneath the magic. Zepto’s challenge is therefore not to prove that India wants quick commerce. That question has already been substantially answered. The challenge is to prove that Indian quick-commerce demand can be served at margins that justify a premium valuation.

Quick commerce trained India to admire speed. The IPO market will now ask whether speed is a moat, or merely a costly service standard that every serious player must subsidise.

Final Institutional Verdict

Zepto is not an obvious failure story. It is far more interesting than that. It is a company with genuine consumer traction, extraordinary growth, major brand visibility, a large capital base and a credible shot at becoming India’s first pure-play quick-commerce listing. But it is also a company whose FY25 numbers show that scale was bought at enormous cost, and whose FY26 story now depends on proving that burn reduction is structural rather than cosmetic.

The updated DRHP will decide the argument. If Zepto shows mature-store economics, improving contribution margins, rising AOV, monetisable advertising, lower promotional intensity and sustainable order growth on a stable dark-store base, then the IPO becomes a disciplined growth story. If the numbers show that order growth still depends heavily on discounts, free delivery and capital-funded frequency, then the IPO becomes a public-market transfer of a private-market subsidy model.

The verdict, for now, is precise: Zepto has not failed the quick-commerce thesis, but it has not yet cleared the public-market test of the quick-commerce thesis. FY25 exposed the burn. FY26 claims repair. The DRHP must prove the repair. That is the next Projection Gap.