The market has started to discover that artificial intelligence is not weightless.

For two years, the AI trade was described through chips, models, data, cloud revenue and productivity. That description was not wrong, but it was incomplete. It treated artificial intelligence as if it were a software cycle sitting safely above the physical economy. The Iran war and the oil shock have exposed the missing layer.

AI does not only require code. It requires power. It requires transmission. It requires cooling. It requires gas turbines, transformers, substations, land, water, permits, backup fuel and grid capacity. Once energy becomes unstable, the AI trade stops being only a technology story. It becomes an infrastructure story with commodity risk inside it.

That is the quiet repricing now beginning inside markets.

Brent crude touched 126.41 dollars a barrel in late April as investors priced the risk of a prolonged US Iran war and persistent disruption around the Strait of Hormuz. In the same week, AI linked equities began showing stress. AP reported that Broadcom fell 4.4 percent, Nvidia 1.6 percent and Micron 3.9 percent while the Nasdaq slipped from record levels. The movement was not yet a regime break. It was an early warning.

Oil risk is creeping into tech valuations because AI has moved from digital scarcity to physical scarcity.

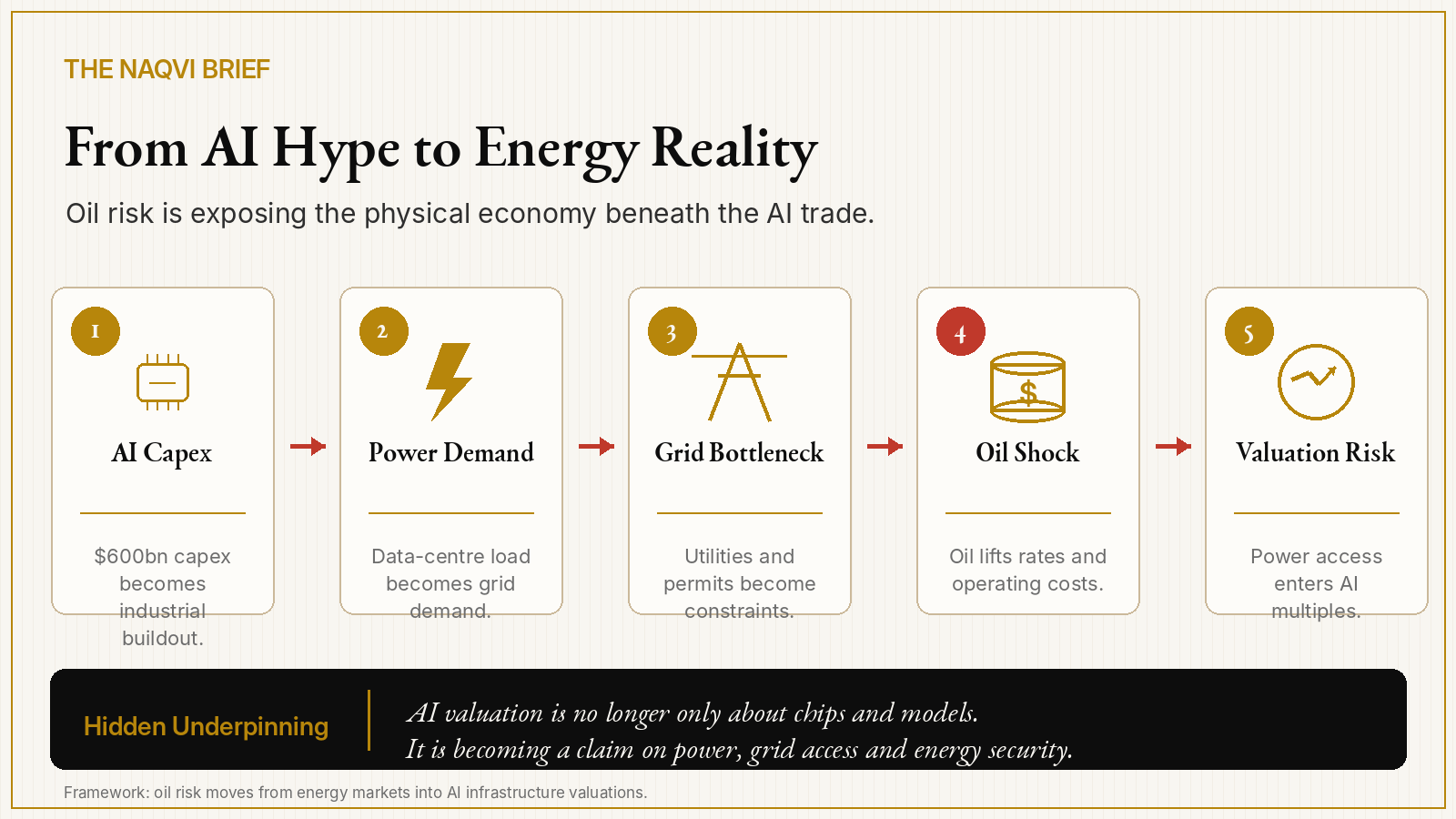

The first layer is capital expenditure.

Reuters reported that Amazon, Meta, Microsoft and Alphabet are on track to spend roughly 600 billion dollars on AI this year. That is not normal software investment. It is industrial mobilisation. Data centres, chips, networking equipment, cooling systems and power infrastructure are now being funded at a scale closer to strategic buildout than ordinary corporate expansion.

The market tolerated that spending because it believed the payoff would arrive through cloud revenue, model monetisation, enterprise adoption and productivity gains. But energy shock changes the equation. If power costs rise, if grid connection delays lengthen, if gas turbine supply tightens, if utilities require larger capital plans, then AI infrastructure spending becomes heavier and slower to convert into free cash flow.

The AI multiple was built on the assumption that scale would unlock margin. The energy shock introduces the opposite possibility: scale may first unlock more fixed cost.

The second layer is electricity demand.

The International Energy Agency projects global electricity consumption from data centres to roughly double from 485 terawatt hours in 2025 to 950 terawatt hours in 2030, accounting for around 3 percent of global electricity demand by then. It also expects electricity use from AI focused data centres to triple over the same period.

This is the number that changes the conversation. Data centres are no longer marginal loads hidden inside commercial electricity demand. They are becoming visible loads that force utilities, regulators and governments to make allocation decisions.

In the United States, the EIA expects power demand to rise from a record 4,195 billion kilowatt hours in 2025 to 4,244 billion kilowatt hours in 2026 and 4,381 billion kilowatt hours in 2027. Reuters reported that AI and crypto data centres are a major driver of the increase.

The market may still call AI a software revolution. The grid does not.

The third layer is utility infrastructure.

Entergy increased its four year capital spending plan by about 33 percent to 57 billion dollars, largely because of energy infrastructure needed to serve Meta data centres. Reuters reported that the deal involves seven new natural gas fuelled power plants with more than 5.2 gigawatts of capacity, while Entergy also sees another 7 to 12 gigawatts of potential data centre customers.

That is the real AI supply chain. Not only Nvidia. Not only memory. Not only servers. The supply chain now includes regulated utilities, gas turbines, power contracts, transmission approvals and the politics of who pays for grid expansion.

GE Vernova’s improved outlook points in the same direction. Reuters reported that power hungry AI data centres are boosting orders for gas turbines and grid equipment. The AI boom is therefore already being translated into demand for heavy power hardware.

This is where tech valuations begin to touch energy politics. A hyperscaler can buy chips. It cannot always buy grid capacity at the speed its valuation assumes.

The fourth layer is the oil shock itself.

The World Bank expects energy prices to rise 24 percent in 2026 even if the most acute Middle East disruption ends in May, and warned that prices could rise further if the war persists. That is a direct macro input into the AI trade because high energy prices change inflation expectations, interest rate assumptions, utility capex, construction costs and corporate margins.

Oil does not need to power every data centre directly to reprice AI. It only needs to affect the macro conditions under which AI infrastructure is financed and operated.

Higher oil can lift inflation. Higher inflation can delay rate cuts. Higher rates reduce the present value of long dated AI cash flows. Higher energy costs raise the cost base of data centre ecosystems. Higher commodity volatility forces investors to ask whether the AI trade deserves the same multiple when its physical inputs are no longer stable.

This is not correlation. It is transmission.

The fifth layer is valuation discipline.

The AI trade has been priced as if compute scarcity creates pricing power. But a second scarcity is emerging beneath it: power scarcity. If electricity, grid access and energy security become binding constraints, the winners may not be the companies with the most aggressive model roadmaps. They may be the companies with the most secure power strategy.

This shifts the investment lens. Data centre operators with power access become more valuable. Utilities near AI clusters gain strategic importance. Gas turbine manufacturers, grid equipment suppliers and power infrastructure firms become hidden AI beneficiaries. At the same time, highly valued AI names that consume capital without proving durable cash generation face sharper scrutiny.

The AI trade is not dead. That is not the argument. The argument is more precise: AI is being dragged from narrative finance into physical economics.

The second order effect is geopolitical.

If AI is strategic infrastructure, then energy supply becomes part of technological sovereignty. Countries that control cheap, reliable electricity will have an AI advantage. Countries with congested grids, fuel vulnerability or slow permitting will discover that model ambition is not enough.

The United States can still lead the AI race. But leadership will now depend on more than semiconductors and venture capital. It will depend on whether America can build power plants, transmission lines and grid connections fast enough to match the speed of its AI capital expenditure.

China understands this instinctively because industrial power has always been central to its state capacity. The Gulf understands it because energy is its native language. Europe is the most exposed because it wants AI sovereignty but still carries the scars of energy insecurity. India’s question is different: can it turn rising electricity demand into strategic advantage before grid stress turns into a constraint?

The AI race is becoming an energy race.

The market is only beginning to price this.

For now, investors still treat oil shocks as macro noise and AI as a secular growth story. But the distinction is weakening. Once data centres become city scale loads and hyperscaler capex becomes a 600 billion dollar infrastructure cycle, energy prices are no longer outside the technology trade. They sit underneath it.

The next AI correction may not begin with a model failure. It may begin with a power constraint, a delayed grid connection, a gas turbine shortage, a regulatory fight over who pays for infrastructure, or an oil shock that keeps rates higher for longer.

That is why the war is repricing AI.

It is forcing the market to admit that the future of intelligence still runs through the old economy: barrels, wires, turbines, steel and grids.

The deeper shift is not that oil directly powers AI. It is that AI has become so physically large that energy volatility now enters its valuation architecture.

When compute turns into infrastructure, the market must price not only models and chips, but electricity, grid access, fuel security and the cost of capital.

IEA projections on data-centre electricity demand; Reuters reporting on EIA power demand forecasts, World Bank energy-price risks, hyperscaler AI spending, Entergy’s Meta-linked capex expansion, GE Vernova’s AI-driven power equipment outlook, and AP reporting on AI stocks falling alongside rising oil prices.