Urban Company was supposed to be the cleaner Indian startup story: not the wildest, not the loudest, not the most glamorous, but one of the few platform companies that seemed to have crossed the psychological line from venture-capital burn to public-market discipline. It had brand trust, category depth, trained professionals, operating history, a listed-market presence, and a far more credible path to profitability than many consumer internet peers.

That is precisely why the latest numbers matter. Urban Company’s Q4 FY26 revenue from operations rose about 43% year-on-year to roughly ₹426 crore, but its consolidated quarterly net loss widened to about ₹161 crore from around ₹2.8 crore a year earlier. For FY26, the company reportedly moved from a ₹240 crore net profit in FY25 to a ₹235 crore net loss, even as full-year revenue rose 36% to ₹1,556 crore and net transacting value rose 31% to ₹4,290 crore.

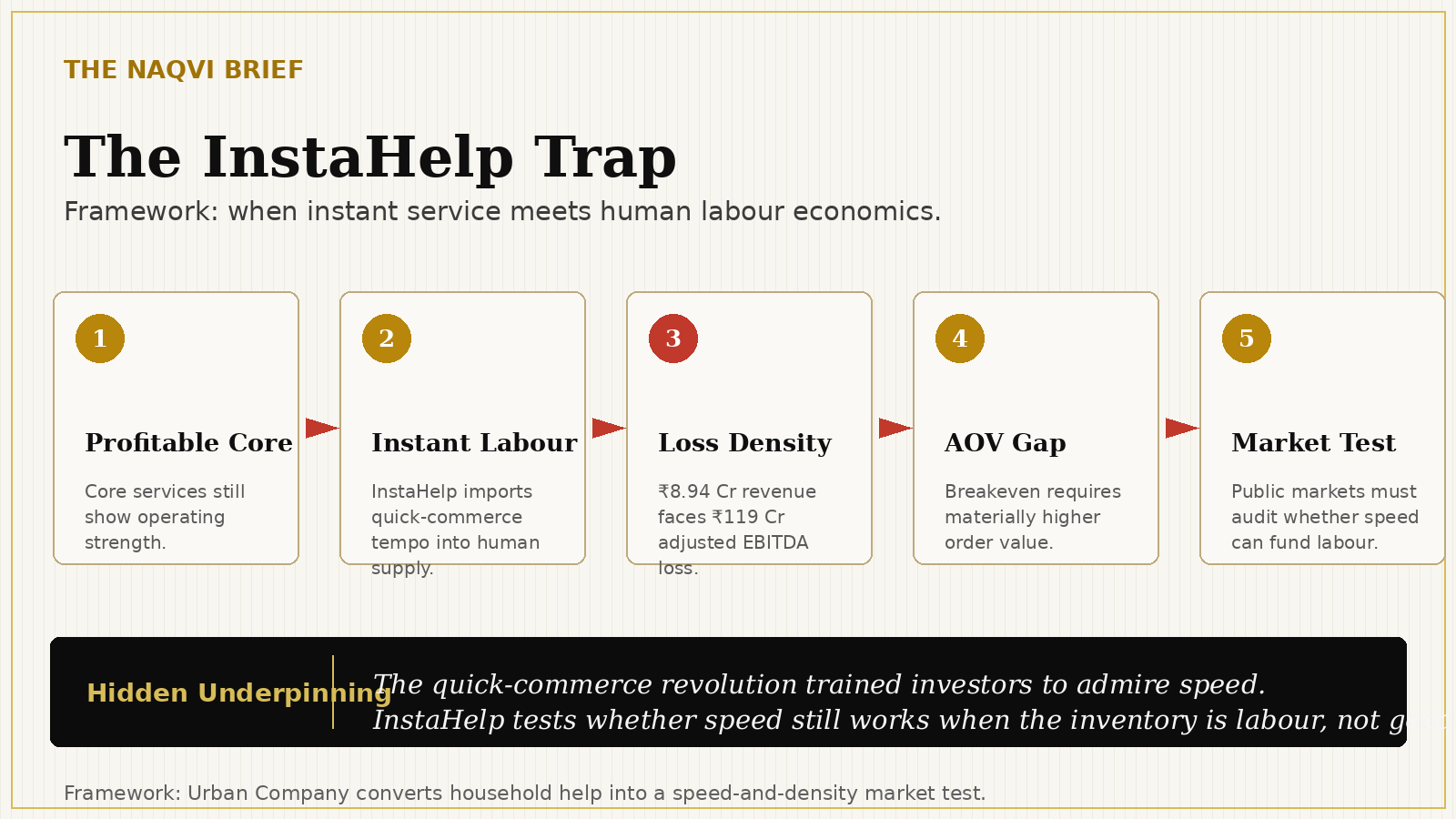

This is not the usual startup story of a loss-making company promising future profits. It is more uncomfortable than that. Urban Company had already shown the market what profitability could look like. Then it chose to re-enter the burn cycle through InstaHelp, its quick-service household-help vertical.

The Financial Autopsy

| Metric | Earlier Period | Current Period | Change | Forensic Reading |

|---|---|---|---|---|

| Q4 revenue from operations | ₹298 Cr | ₹426 Cr | +43% | Growth remains strong |

| Q4 net loss | ₹2.8 Cr | ₹161 Cr | 57x wider | Profit discipline broke sharply |

| FY25 net result | ₹240 Cr profit | ₹235 Cr loss in FY26 | ₹475 Cr swing | Public-market profitability story reversed |

| FY26 revenue from operations | ₹1,144 Cr in FY25 | ₹1,556 Cr | +36% | Revenue growth did not protect bottom line |

| FY26 NTV | Around ₹3,275 Cr implied | ₹4,290 Cr | +31% | Marketplace scale expanded |

| Q4 InstaHelp revenue | New vertical | ₹8.94 Cr | Early scale | Revenue still tiny |

| Q4 InstaHelp adjusted EBITDA loss | New vertical | About ₹119 Cr | Severe burn | New category consuming profitability |

| Q4 adjusted EBITDA excluding InstaHelp | Reported positive | ₹22 Cr | Core remains healthy | Problem is not the old engine |

The first reading is obvious: Urban Company grew strongly. The deeper reading is more important: the company’s mature core appears healthier than the headline loss suggests, but the InstaHelp experiment has reintroduced a venture-style loss engine inside a company that had already trained investors to expect profitability. This distinction matters because this is not a collapse of Urban Company’s entire operating model. It is a capital-allocation question. The company has not lost its core; it has chosen to subsidise a new battlefield.

The Original Capital-Market Thesis

Urban Company’s thesis was built on professionalisation, not chaos. The company was supposed to organise India’s fragmented home-services market by converting unreliable local labour into a managed, trained, rated and repeatable service marketplace. The promise was not merely convenience. The promise was trust at scale.

This was a better-quality platform thesis than many Indian consumer internet stories because the problem was real. Customers did not only want cheaper services; they wanted predictable service quality, safety, scheduling reliability and accountability. Service professionals did not only want gigs; they wanted access to demand, training, brand credibility and better utilisation.

That model could justify a premium if three conditions held: customer trust improved with scale, provider utilisation improved with density, and operating discipline improved as repeat categories matured. Urban Company’s core numbers suggest that this original engine may still be functioning. The issue is that InstaHelp changes the economic character of the company. It is not simply another home-service category. It is an attempt to import the quick-commerce tempo into human labour, and that is a different risk category.

The InstaHelp Trap

Quick commerce works because inventory can be pre-positioned. A packet of milk, a phone charger or a shampoo bottle can sit inside a dark store and wait for demand. Human labour cannot be warehoused in the same way. This is the central difference.

Instant household help requires live human availability, hyperlocal density, trust, training, scheduling, wages, cancellations, repeat behaviour and two-sided reliability. The customer wants immediacy. The worker wants adequate earnings. The platform wants margin. These three demands do not automatically align.

In Q4 FY26, InstaHelp reportedly handled about 2.7 million orders and ₹40 crore of NTV, up from 1.6 million orders and ₹28 crore of NTV in Q3 FY26. On the surface, that looks like strong sequential growth. But when the same vertical generates only about ₹8.94 crore in revenue while producing roughly ₹119 crore in adjusted EBITDA loss, the forensic question is not whether orders are growing. The question is what each order is actually costing the company.

Using the reported Q4 numbers, InstaHelp’s NTV per order was roughly ₹148, revenue per order was about ₹33, and adjusted EBITDA loss per order was roughly ₹440. These are approximate calculations from reported order volume, NTV, revenue and adjusted EBITDA loss, but they expose the problem clearly: the company may be buying density at a cost that is far heavier than the early revenue base can support. The real issue is that Urban Company is trying to create instant-service density in a category where the unit of supply is not a product, but a human being.

The AOV Problem

Urban Company has already indicated that InstaHelp’s average order value may need to rise about 1.8 to 2 times to reach breakeven. That statement is crucial because it reveals that the current problem is not merely early-stage marketing spend. The category’s revenue architecture itself may be too thin at present order values.

If average order value must nearly double, the platform faces a difficult consumer question: will Indian households pay enough for instant domestic help to support worker economics, platform take-rate, service quality, training, onboarding and marketing? Indian consumers may love speed, but that does not mean they will pay enough for speed when the service involves labour rather than packaged goods. The quick-commerce analogy becomes dangerous because grocery urgency and domestic-help urgency have different willingness-to-pay curves.

The company can raise prices, but that may slow adoption. It can subsidise demand, but that extends burn. It can reduce worker payouts, but that weakens supply quality. It can compress platform margin, but that delays profitability. Every route carries pain.

The Advertisement of Growth vs The Arithmetic of Density

Urban Company’s management has framed the loss expansion as strategic investment to win InstaHelp. CEO Abhiraj Singh Bhal reportedly said the company is “playing to win” and is not playing merely “to look elegant”, while the company is investing to capture market share in the category. That may be strategically rational, but public-market investors must separate strategic aggression from economic inevitability.

A company can be right to invest and still wrong about the eventual profit pool. The question is not whether InstaHelp can become large. The question is whether it can become large at acceptable margins. Reports point to rising competition from Pronto and Snabbit, which means Urban Company is not scaling InstaHelp in a vacuum. It is entering a category where customer acquisition, partner onboarding and incentive pressure may remain elevated for longer than the market expects.

If the competitive environment forces every player to subsidise speed, then the market may grow while the profit pool remains shallow. That is exactly the kind of illusion The Projection Gap is designed to detect.

The Core Business Is Not the Problem

A fair autopsy must say this clearly: Urban Company is not Ola Consumer. Ola’s problem is that the core mobility engine itself contracted sharply before the FY26 repair claim. Urban Company’s problem is different. Its core business appears to have strength, while a new vertical is consuming the profitability that the core had started to produce.

This distinction makes Urban Company a more sophisticated case. It is not a failing company trying to invent a future. It is a company with a credible core choosing to fund a high-burn future category. That makes the management decision more important than the headline loss.

If InstaHelp becomes a durable high-frequency household-services layer, Urban Company may have opened a major new growth engine. If InstaHelp remains subsidy-dependent, the company may have taken a profitable platform and dragged it back into a private-market style cash-burn race after entering public-market scrutiny.

The Global Parallel: Quick Commerce Without Inventory

The natural comparison is not Uber or Ola. It is quick commerce. Quick commerce taught Indian consumer internet a seductive lesson: if delivery becomes fast enough, habit formation accelerates. Blinkit, Zepto, Swiggy Instamart and others showed that speed can change consumer behaviour. But those models are inventory-led, route-optimised and dark-store dependent.

InstaHelp is different because the “inventory” is time, trust and labour. The platform cannot simply increase shelf availability. It must ensure human availability at the right location, at the right time, with acceptable skill, acceptable conduct, acceptable pay and acceptable customer experience. That makes the scaling problem far more complex.

A dark store can hold inventory even when demand fluctuates. A worker cannot be infinitely idle without cost or dissatisfaction. This is why instant labour marketplaces may face a harsher density equation than instant grocery. They need enough demand to keep workers utilised, enough supply to keep wait times low, and enough pricing power to fund the gap between the two. That triangle is not easy.

The Capital-Market Question

The most important market question is not whether Urban Company can afford the burn. Reports suggest the company ended FY26 with a strong cash position, including commentary that it remains positioned to fund the current burn phase. The more important question is whether the burn deserves a premium multiple.

Public markets treat investment burn differently from repair burn. If InstaHelp burn is creating a defensible category, investors may tolerate it. If it is merely matching competitor subsidies, the same burn becomes value leakage.

This is where Urban Company must provide sharper disclosures. Investors need to see city-level contribution margins, repeat cohorts, pricing progression, partner retention, order density, cancellation rates, average order value movement and incentive intensity. Without these, the market is being asked to trust a category narrative while the numbers are still deeply negative. That is not enough for a public company.

Status Quo Projection: 3 to 5 Years

| Scenario | Probability | What Happens | Investor Meaning |

|---|---|---|---|

| Best Case | 25% | InstaHelp scales, AOV rises, worker density improves and losses narrow materially by FY28 | Urban Company becomes India’s dominant managed home-services platform |

| Base Case | 45% | Core remains profitable, but InstaHelp keeps absorbing profit for several years | Valuation multiple stays capped despite revenue growth |

| Bear Case | 25% | Competition forces continuing subsidies, AOV does not rise enough and the vertical remains structurally loss-making | Market begins treating InstaHelp as a drag rather than a growth engine |

| Systemic Risk Case | 5% | Instant labour services become another consumer-tech subsidy war with limited profit pools | Public markets reprice quick-service models below quick-commerce enthusiasm |

The base case is not collapse. The base case is profit deferral. Urban Company may keep growing and still disappoint investors if the new vertical delays consolidated profitability for too long.

The Recovery Roadmap

Urban Company does not need to abandon InstaHelp. It needs to discipline the story before the story disciplines the stock. First, the company should publish category-level unit economics with greater clarity. NTV, revenue, adjusted EBITDA loss and order count are useful, but the market needs cohort retention, city maturity curves, AOV progression, partner utilisation, incentive intensity and repeat-order behaviour.

Second, the company should cap the acceptable burn per order and show a planned glide path. A category that loses hundreds of rupees per order cannot be defended indefinitely through “market-share capture” language. Third, the company must separate mature-city economics from expansion-city economics. If older cities show improving contribution while new cities absorb losses, investors can understand the curve. If all cities remain heavily negative, the thesis weakens.

Fourth, Urban Company must avoid blindly copying quick-commerce psychology. The company should not confuse instant fulfilment with instant profitability. Household labour is not a packet of groceries. Fifth, it should build subscription and recurring-use products around InstaHelp rather than relying only on impulse demand. Recurring weekly cleaning, trusted household support plans, building-level partnerships and corporate residential tie-ups may create better utilisation than one-off instant bookings.

The deeper issue is that Indian consumer internet has discovered a new temptation: after quick commerce, every category now wants to become “instant”. But not every category can support instant economics.

Speed is expensive. In inventory-led commerce, speed is funded through dark-store density, supplier terms, basket size and logistics optimisation. In labour-led services, speed must be funded through human availability, idle-time management, trust systems, training and local density.

This makes InstaHelp a test case for a broader question: can India’s instant economy extend from products to people without destroying unit economics? That question is much larger than Urban Company. It touches domestic work, gig labour, urban households, platform intermediation, women’s workforce participation, service trust, labour formalisation and public-market discipline. If Urban Company solves it, the company may create one of India’s most important managed-services categories. If it fails, InstaHelp may become proof that the instant-economy thesis breaks when the underlying supply is human time.

The quick-commerce revolution trained investors to admire speed. InstaHelp will test whether speed still works when the inventory is labour, not goods.

Final Institutional Verdict

Urban Company’s latest numbers do not show a broken company. They show a profitable-core company taking a dangerous public-market bet on a new high-burn category. That is why the story deserves the homepage.

The old Urban Company thesis was disciplined: trust, training, repeat services and organised home-service supply. The new InstaHelp thesis is more aggressive: instant household help, faster density, higher frequency and market-share capture before competitors harden. The first thesis was about professionalisation. The second is about speed. The risk is that speed may consume the economics that professionalisation created.

Urban Company may still be right. InstaHelp may mature, AOV may rise, cohort behaviour may improve, and losses may compress as density deepens. But the burden of proof has shifted. After FY26, the company can no longer rely only on the credibility of its core platform. It must prove that InstaHelp is not another subsidy-led consumer-tech race hiding behind the language of category creation.

The market should not punish ambition. But it must audit the arithmetic of ambition. For now, the verdict is clear: Urban Company remains one of India’s better platform businesses, but InstaHelp has turned it into a live experiment in whether instant labour can ever produce public-market grade economics. That is the next Projection Gap.