Ola Electric is not merely another weak quarterly result story. It is a much larger test of whether India’s startup-style EV revolution can survive the hard industrial realities of manufacturing, service quality, working capital, warranty confidence, retail execution and capacity utilisation.

The company’s own language now calls FY26 a reset year. That word matters. A reset is not a victory lap. It is an admission that the earlier operating model had to be repaired. Ola Electric says FY26 was focused on strengthening service, product quality, gross margins, operating costs, cash discipline, sales productivity and cell manufacturing. The company also says Q4 FY26 showed the reset working, with gross margin expanding, operating cash flow turning positive and service stabilising.

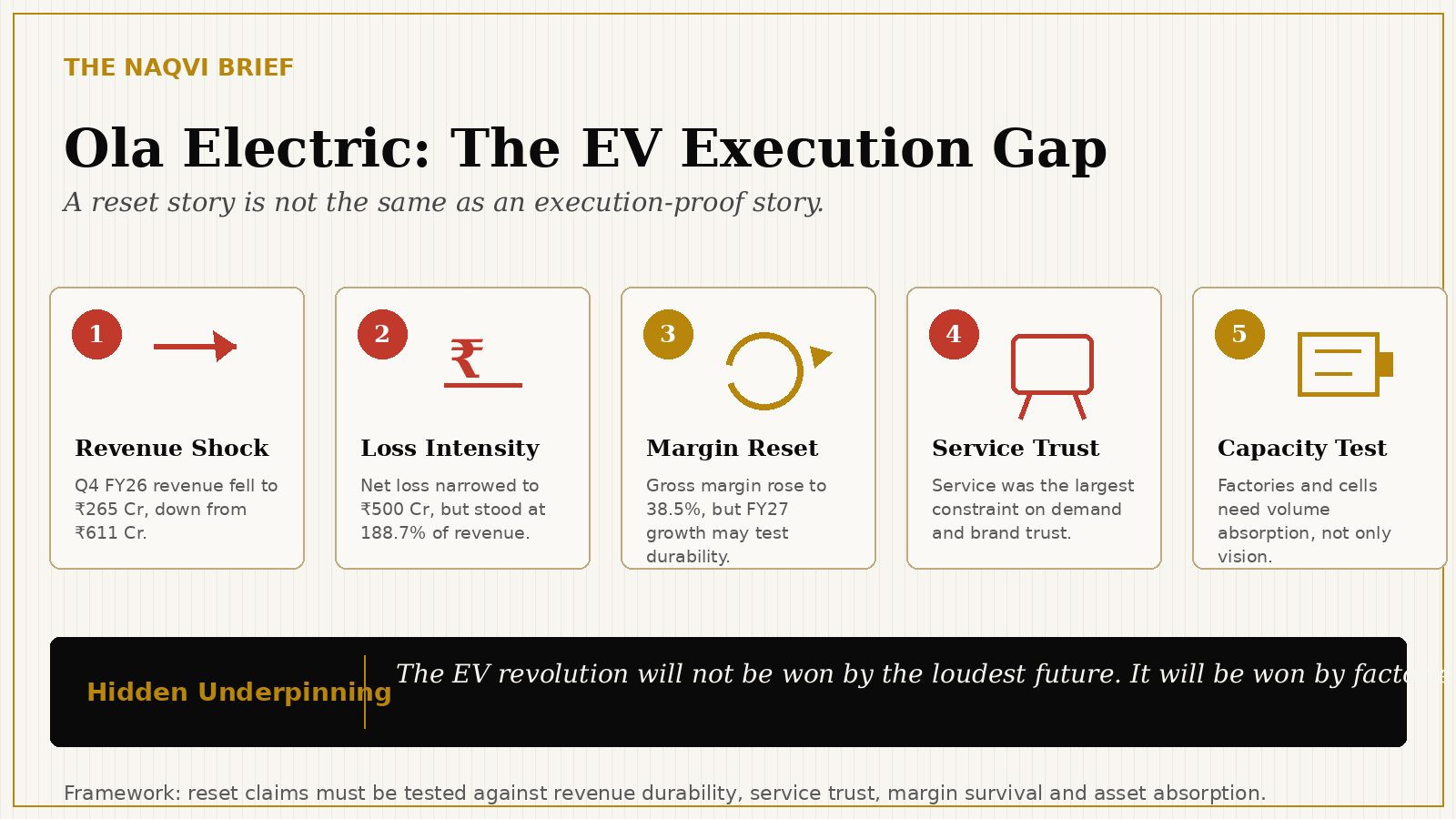

That is the bull case. The bear case is in the same result. Ola Electric’s Q4 FY26 revenue from operations was only ₹265 crore, down from ₹611 crore in Q4 FY25. Deliveries fell from 51,375 units in Q4 FY25 to 20,256 units in Q4 FY26. Revenue fell about 56.6%, while delivery volume fell about 60.6%. Net loss narrowed from ₹870 crore to ₹500 crore, but that improvement came against a much smaller revenue base.

That is the uncomfortable arithmetic. In Q4 FY25, the company lost about ₹142 for every ₹100 of revenue. In Q4 FY26, despite lower absolute losses, loss intensity worsened because the topline collapsed faster than the loss base. The market was told to admire cost discipline. The forensic audit must ask why the business still produced losses nearly 1.9 times its quarterly revenue.

The Financial Autopsy

| Metric | Q4 FY25 | Q4 FY26 | Change | Forensic Reading |

|---|---|---|---|---|

| Revenue from operations | ₹611 Cr | ₹265 Cr | -56.6% | Topline collapse |

| Deliveries | 51,375 units | 20,256 units | -60.6% | Demand and execution pressure visible |

| Net loss | ₹870 Cr | ₹500 Cr | Improved 42.5% | Cost cuts helped, but loss remains large |

| Net loss as % of revenue | 142.4% | 188.7% | Worse | Loss intensity deteriorated |

| Gross margin | 13.7% | 38.5% | +24.8 pp | Product economics improved sharply |

| Operating expenses | ₹844 Cr | ₹428 Cr | -49.3% | Cost base reset is real |

| Q4 operating CFO | Negative earlier | ₹91 Cr positive | Improved | Cash discipline improved |

| Q4 FCF | NA | -₹131 Cr | Still negative | Cash story not fully repaired |

| FY26 revenue | NA | ₹2,253 Cr | Reset-year base | Scale far below manufacturing ambition |

| FY26 deliveries | NA | 173,794 units | Reset-year base | Capacity utilisation question remains |

This table is the entire Ola Electric story. The company improved gross margin, reduced operating expenses sharply and turned operating cash flow positive in Q4 FY26. Those are not trivial achievements. But the same period also shows severe revenue compression, collapsed deliveries and a loss-to-revenue ratio that remains structurally alarming. A proper Projection Gap story must hold both truths at once: Ola Electric may have repaired parts of the cost structure, but it has not yet proved that the demand engine, service engine and manufacturing engine can scale together.

The Original Capital-Market Thesis

Ola Electric’s original public-market thesis was not modest. It was never only about selling scooters. It was about building India’s vertically integrated electric mobility platform: two-wheelers, motorcycles, software, batteries, cells, manufacturing, charging, energy storage and eventually a broader electric ecosystem.

The company argued that deep vertical integration would create structural advantage across motors, batteries, cells, electronics and software. In earlier shareholder communication, Ola Electric described a manufacturing footprint that could support 1 million vehicles and 6 GWh of cell capacity. It also described a revenue potential of ₹15,000 crore to ₹20,000 crore over the next few years. That is the promise. The Q4 FY26 numbers show the gap.

If the manufacturing footprint supports 1 million vehicles, but FY26 deliveries were 173,794 units, the company is still far from growing into the industrial base it has created. A factory can be a strategic asset when volume scales. It becomes an under-absorbed cost burden when demand, service execution or market confidence slows.

The Reset Claim

The company’s strongest argument is that FY26 was deliberately not optimised for short-term volume. Ola Electric says it chose to realign its retail footprint, cost structure and operating model to a more sustainable steady state. This is a plausible explanation, but public-market investors must distinguish between three different things: a temporary volume sacrifice to repair fundamentals, a structural fall in demand due to damaged brand trust, and a competitive loss of market position.

The first is bullish. The second is dangerous. The third is valuation-destructive. The central audit question is therefore precise: is Ola Electric voluntarily resetting from a position of strength, or repairing from a position of damaged market confidence?

The Service Trust Problem

The most important operating sentence in the company’s Q4 press release is not about gross margin. It is about service. Ola Electric itself said service was the largest constraint on demand and brand trust through FY26, and that it had materially stabilised by Q4.

The company reported that average service turnaround time fell by 88%, from around 9 days in October 2025 to nearly 1 day in March 2026. It also reported that service backlog reduced from 14 days to 6 days, same-day closures improved to nearly 87%, and parts pendency reduced by 69% from October to April. This is positive, but it is also revealing.

A software company can recover from bugs quickly. A vehicle company cannot treat service failure as a minor friction point. In automobiles, service is not after-sales support. Service is product trust. It affects resale value, referral behaviour, financing confidence, fleet adoption, brand reputation and regulatory comfort.

The Gross Margin vs Volume Paradox

Ola Electric’s gross margin improvement is real. Consolidated gross margin expanded to 38.5% in Q4 FY26 from 13.7% in Q4 FY25. The company says this reflects vertical integration, Gen 3 platform maturity, pricing architecture and downstream control. It also says gross margin excluding PLI stood at 33.5%.

That is impressive on paper. But gross margin at low volume is not the final proof of industrial economics. The real test is whether Ola Electric can maintain strong gross margins while volumes recover, pricing investments return, commodity inflation affects costs and competition intensifies. The company itself expects Q1 and Q2 FY27 margins to moderate from Q4 levels due to commodity inflation and pricing investments to accelerate growth.

Q4 FY26 may show repaired product economics, but FY27 will test whether those economics survive growth. A business can look disciplined when it cuts volume, reduces expenses and slows aggression. It becomes a true industrial compounder only when it scales without reopening the old loss structure.

The Capacity Utilisation Question

Ola Electric’s industrial ambition is large. The company says its Gigafactory has 2.5 GWh operational capacity, with installation to 6 GWh largely complete, and commercialisation expected to be completed by the end of the quarter. It also says the cell platform is being built around auto and external cell sales, Shakti and Mahashakti, with captive cell consumption expected to scale to 1.5 to 2 GWh by FY27 exit.

This is the upside story. If internal cells reduce costs, improve supply security and support storage products, the company can potentially create a real manufacturing moat. But the capacity question remains. Heavy industrial assets require absorption. If volumes do not recover meaningfully, the very integration that was supposed to create advantage can create operating pressure.

Vertical integration is powerful when demand is large and stable. It is dangerous when demand is volatile and utilisation is weak. This is why Ola Electric cannot be valued only as an EV brand. It must be audited as a manufacturing system.

The Competitive Reality

The electric two-wheeler market is no longer a blank field waiting for one founder-led brand to dominate. Ola faces competition from incumbents, specialist EV manufacturers and traditional two-wheeler companies with dealer networks, service infrastructure and decades of customer trust.

If Ola Electric must cut prices to recover demand, then the gross margin story faces pressure. If it must invest in service to restore trust, then operating costs face pressure. If it must keep funding cell manufacturing and storage products, then capital requirements remain high. The company is trying to repair all three at once: demand, service and manufacturing scale. That is not impossible, but it is execution-heavy.

The Market Reaction

The market understood the contradiction. Economic Times reported that Ola Electric shares declined after the Q4 FY26 results, while Emkay warned of up to 35% further downside following the sharp revenue slump. That does not make the brokerage automatically right, but the reaction shows that investors are no longer buying EV vision without operating proof.

Public markets are not asking whether India needs electric mobility. That answer is yes. They are asking whether Ola Electric can profitably execute the EV transition at scale. That is a different question.

Unit-Economic Reconstruction

| Unit-Economic Proxy | Q4 FY26 Signal | Interpretation |

|---|---|---|

| Revenue from operations | ₹265 Cr | Revenue base sharply compressed |

| Deliveries | 20,256 units | Volume reset is severe |

| Gross margin | 38.5% | Product economics improved materially |

| Gross margin ex-PLI | 33.5% | Improvement not entirely subsidy-dependent |

| Operating expenses | ₹428 Cr | Cost reset is real |

| Net loss | ₹500 Cr | Business remains deeply loss-making |

| Loss / revenue | 188.7% | Loss intensity remains severe |

| Operating CFO | ₹91 Cr positive | Working-capital and cash discipline improved |

| FCF | -₹131 Cr | Full cash repair incomplete |

| Q1 FY27 order expectation | Nearly 45,000 units | Recovery claim must be verified |

The reconstruction shows why this is not a clean collapse story and not a clean recovery story. It is a repair claim under industrial stress. Ola Electric has improved gross margins, reduced operating expenses and stabilised service metrics. But the company still needs to prove that these improvements can survive volume recovery.

The “Where Does The Cash Come From?” Test

| Cash Source | What Must Be True | Risk |

|---|---|---|

| Scooter volumes | Demand recovers sustainably | Service trust and competition may limit recovery |

| Motorcycles | Roadster becomes a second growth engine | Execution risk in a new subcategory |

| Gross margin | Gen 3 and vertical integration hold | Pricing cuts and commodity inflation may reduce margin |

| Internal cells | Cell economics scale reliably | Manufacturing ramp risk and capital intensity |

| PLI | Incentives support margins | Policy dependence and compliance risk |

| Opex reduction | Leaner model persists | Underinvestment in service or sales may hurt growth |

| Storage products | Shakti and Mahashakti become real demand engines | Adjacent business may require new execution muscle |

The best version of Ola Electric is a vertically integrated EV and energy-storage manufacturer with strong margins, improving service trust, internal battery economics and disciplined operating leverage. The weaker version is a company that built industrial capacity ahead of durable demand, then had to shrink into a reset while competitors gained ground.

Status Quo Projection: 3 to 5 Years

| Scenario | Probability | What Happens | Investor Meaning |

|---|---|---|---|

| Best Case | 25% | Service recovery holds, Q1 FY27 orders double, margins moderate but remain strong, and internal cells improve long-term economics | Ola Electric grows into its manufacturing base and regains investor confidence |

| Base Case | 45% | Volumes recover partially, margins moderate, losses narrow slowly and the company remains a high-execution EV turnaround | Valuation remains capped until sustained delivery growth returns |

| Bear Case | 25% | Competition gains share, price cuts pressure margins, service trust remains fragile and capacity stays underutilised | Market reprices Ola as an overbuilt EV manufacturer |

| Systemic Risk Case | 5% | India’s EV two-wheeler market remains subsidy-sensitive and low-margin despite penetration growth | Sector multiples compress and investors favour incumbents with service depth |

The base case is not bankruptcy. The base case is a long credibility repair cycle. Ola Electric may improve and still disappoint investors if the public market decides that manufacturing execution deserves a lower multiple than EV revolution rhetoric.

The Recovery Roadmap

Ola Electric does not need more vision. It needs proof of repeatable execution. First, the company must publish service metrics consistently across quarters. Turnaround time, backlog, parts pendency and same-day closures should not appear only during a reset narrative. They should become permanent investor metrics.

Second, the company must prove that Q4 gross margin can survive growth. If Q1 and Q2 FY27 margins moderate as expected, investors must see whether volume recovery compensates through operating leverage. Third, Ola must show capacity utilisation economics. A 1 million vehicle manufacturing footprint and 6 GWh cell capacity can be an advantage only if demand scales into the asset base.

Fourth, it must separate Auto and Cell economics clearly. The Auto business reportedly delivered positive CFO and FCF in Q4 FY26, while the Cell business remained in planned investment mode. Investors need to see whether the cell business becomes margin-accretive or remains a capital sink. Fifth, Ola Electric must stop being evaluated as a startup with factories. It must behave like an industrial company with a technology advantage.

The deeper issue is that India’s EV transition has been sold with startup language, but it will be won through industrial discipline.

Electric mobility is not an app category. It is not quick commerce. It is not ride-hailing. It is manufacturing, supply chains, service networks, batteries, software, warranty, financing, customer trust, regulatory compliance and capital allocation fused into one execution system.

The EV revolution will not be won by the company with the loudest future. It will be won by the company that can convert factories, cells, service centres and customers into durable cash flow.

Final Institutional Verdict

Ola Electric’s Q4 FY26 numbers do not show a finished company. They show a company attempting a serious repair after a damaging operating cycle. The repair has evidence. Gross margin improved sharply. Operating expenses were nearly halved. Operating cash flow turned positive for the first time. Service metrics improved materially. The company expects Q1 FY27 orders to nearly double quarter-on-quarter.

But the gap remains large. Revenue collapsed. Deliveries collapsed. Net loss remained ₹500 crore. Loss intensity worsened as a percentage of revenue. The company’s industrial base still needs sustained volume recovery to justify its ambition.

The verdict is precise: Ola Electric has not failed the EV thesis, but it has not yet cleared the industrial execution test of the EV thesis. FY26 was the reset. FY27 must prove whether the reset was a foundation for disciplined scale, or merely a smaller loss structure built after demand and service trust broke. That is the next Projection Gap.