The prime minister’s appeal to Indians to conserve fuel, avoid non-essential foreign travel, pause gold purchases, reduce cooking oil use and cut fertiliser use was not a small lifestyle sermon. It was the state speaking in the language of household discipline because the external account has entered the household.

In normal politics, leaders ask citizens to consume more. In a war-economy moment, they ask citizens to consume less of the things that leak dollars, raise freight costs, raise fertiliser costs, raise the import bill and weaken the currency firewall.

That is why the speech mattered. It converted petrol, diesel, gold, edible oil and foreign travel from private consumption choices into balance-of-payments behaviour.

But the more dangerous story is not only in West Asia. It is in the Pacific.

The equatorial Pacific is shifting toward El Niño conditions. NOAA’s Climate Prediction Center put the probability of El Niño emerging during May-July 2026 at 82 percent. IRI’s mid-May reading described a rapid transition toward El Niño conditions and placed the probability even higher. Reuters has separately reported that forecasts for a strong El Niño are worrying crop markets across Asia while the Iran war keeps fuel and fertiliser costs under pressure.

This is where India’s problem changes shape.

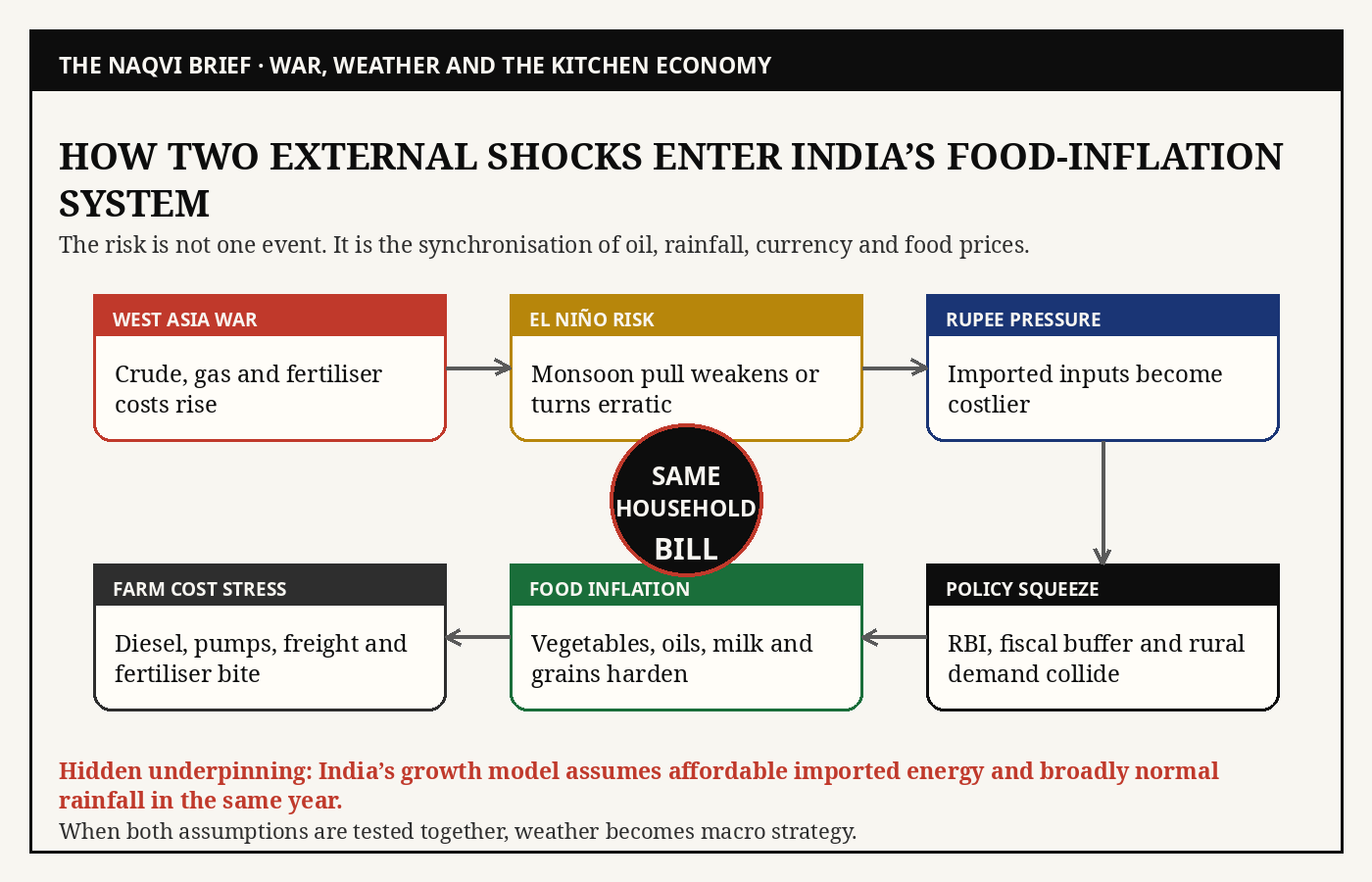

Oil is an external shock. El Niño is a rainfall shock. The rupee is a currency shock. Food inflation is a household shock. India may now be approaching a season in which all four sit on the same table.

The non-obvious risk is not merely that the monsoon may be weak. The non-obvious risk is that India may face a weak monsoon while fuel, fertiliser, freight, edible oil and the rupee are already under stress.

The war hits the pump. El Niño hits the field. The rupee hits the import invoice. Together, they turn weather into macro strategy.

Rain EngineThe monsoon is not weather. It is India’s largest annual liquidity injection.

When it arrives on time and spreads properly, it waters farms, replenishes reservoirs, lowers irrigation stress, supports rural income, stabilises food prices, lowers power pressure and feeds demand into tractors, motorcycles, cement, FMCG, textiles and small-town credit.

When it fails, the transmission is brutal.

Crop stress becomes income stress. Income stress becomes rural demand stress. Rural demand stress becomes factory stress. Food stress becomes inflation stress. Inflation stress becomes RBI stress. RBI stress becomes market stress.

The market calls it rainfall deviation. The economy experiences it as working-capital damage.

India’s monsoon delivers almost 70 percent of the rainfall needed to water farms and refill reservoirs. Agriculture is no longer the largest part of India’s GDP, but it remains one of the largest carriers of Indian livelihood, prices, rural consumption and political stability. That is why the monsoon still behaves like a macroeconomic institution.

A small weather anomaly in the Pacific can therefore become a credit, inflation and fiscal problem in India.

The basic science is simple. In summer, Indian land heats faster than the surrounding ocean. Hot air rises over the subcontinent and creates a low-pressure zone. Moist air from the ocean rushes in to fill that vacuum. That wind carries water. That water becomes the monsoon.

But India’s rainfall engine is not only local. The Pacific matters because normal trade winds push warm water westward toward Indonesia and the western Pacific. That warm pool supports convection and helps maintain a circulation pattern favourable to the Indian monsoon.

During El Niño, the central and eastern Pacific warm unusually. The circulation shifts. The normal wind and pressure pattern weakens or reverses. The monsoon engine loses part of its pull.

Reuters has described the mechanism plainly: El Niño warms the central and eastern Pacific, alters atmospheric circulation and weakens monsoon winds over the Indian subcontinent. Historically, India has received below-average rains in many El Niño years, though not every El Niño produces the same outcome.

That caveat matters. El Niño is not destiny. The Indian Ocean Dipole, intra-seasonal rain distribution, reservoir levels, sowing choices, irrigation coverage and policy response all matter.

But policy must not confuse uncertainty with safety.

Historical LedgerHistory is the warning system.

The Indian monsoon record does not treat drought as a poetic fear. The Indian Institute of Tropical Meteorology's all-India rainfall record identifies 26 major drought years between 1871 and 2015, defined as years when all-India summer monsoon rainfall fell more than 10 percent below the mean. The list includes 1877, 1899, 1918, 1965, 1972, 1982, 1987, 2002, 2004, 2009, 2014 and 2015.

The El Niño connection is not perfect, but it is too strong to ignore. ICRIER's study of El Niño and Indian droughts found that since the 1950s there were 23 global El Niño years and 13 Indian drought years; 11 of those 13 Indian drought years were El Niño years. It also notes that the three severe post-1980 drought years with rainfall more than 15 percent below the long-period average, 1987, 2002 and 2009, were all El Niño years.

More recent drought research carries the same warning. A 2024 Drought Atlas of India ranked the summer monsoon drought of 2002 as the most severe monsoon-season drought in the 1901-2020 record, followed by 1972, 1987 and 1918. These are not dead dates. They are the historical stress tests of India's food, rural income and inflation system.

1877 was the famine warning. 1972 was the growth warning. 1987 was the grain-security warning. 2002 was the GDP warning. 2009 was the inflation warning. 2026 could become the first full-spectrum climate-energy-currency warning.

The point is not that 2026 will repeat 1877. It will not. Modern India has food stocks, state capacity, forecasting systems and welfare architecture that colonial India did not have. The point is sharper: when monsoon weakness arrives in a year of oil stress, rupee pressure and high input costs, history stops being background and becomes an operating manual.

Heat LayerRainfall is only the first channel. Heat is the second.

El Niño is normally associated with higher global temperatures because the warm central and eastern Pacific release heat into the atmosphere and disturb circulation patterns. For India, that means the risk is not only weaker rain. It is also longer heat stress, higher power demand, greater irrigation load, crop moisture stress, labour-productivity loss and faster deterioration of perishables.

A weak monsoon damages the farm. Extreme heat damages the farmer, the grid, the crop and the household budget at the same time.

A central bank can fight inflation. A government can release grain. A trader can hedge oil. A farmer cannot hedge a failed August.Modern Shield

The danger in 2026 is not that India is 1876 again. It is not. India has food stocks, rail networks, meteorological forecasting, public procurement, welfare architecture, fertiliser subsidies, satellite monitoring and a state capacity that colonial India did not have.

That difference is decisive.

Government foodgrain stocks were reported at roughly 604 lakh tonnes against a mandatory buffer norm of about 210 lakh tonnes as of 1 April 2026. This is the hard institutional difference between a climate shock and a famine shock.

But buffer stocks do not irrigate a cotton field. They do not refill a dry well. They do not automatically protect vegetable prices, milk prices, edible oil costs, fodder stress, power demand or rural disposable income.

The old famine risk has been replaced by a modern macro risk: inflation without adequate income, stocks without distribution comfort, and rural stress without fiscal room.

The West Asia war has already moved into India’s macro numbers. Reuters reported that India’s wholesale inflation rose unexpectedly to 8.3 percent in April, the fastest in three-and-a-half years, driven by energy costs from the Middle East crisis. Wholesale fuel and power prices jumped 24.71 percent year-on-year, while petroleum and natural gas prices rose 67.2 percent.

That matters because the food system is fuel-intensive.

Diesel moves tractors, pumps, trucks and mandis. Natural gas feeds fertiliser. Freight moves vegetables, grains, dairy and edible oils. Imported crude affects the rupee. A weaker rupee raises the landed cost of imported inputs. Expensive inputs hit farmers before the crop is even harvested.

Now place a weak or erratic monsoon on top of that system.

The same farmer who needs timely rain may also face higher diesel, higher fertiliser, higher transport, tighter credit and lower demand. The same consumer who pays more for fuel may also pay more for vegetables, edible oil and milk. The same RBI that wants to support growth may be forced to respect the inflation impulse coming from energy and food together.

This is how a conflict outside India and a patch of warm water in the Pacific can meet inside the Indian kitchen.

Kitchen EconomyThe phrase kitchen economy is not soft. It is hard macroeconomics.

Food has a large weight in India’s consumer inflation basket. Fuel has direct and indirect pass-through. Rural wages and rural demand affect volume growth for companies that sell everything from biscuits to two-wheelers. Power demand rises when heat rises and irrigation stress deepens. Bank stress increases when rural cash flows weaken.

A monsoon shock therefore does not stay in agriculture. It moves into inflation expectations, company earnings, fiscal choices, import policy, export curbs, procurement pressure and monetary policy.

India has learned to manage these shocks better than before. But management is not immunity.

The state can ban exports. It can release stocks. It can reduce duties. It can raise duties. It can subsidise fertiliser. It can instruct oil companies. It can intervene in the rupee. It can push conservation. But every intervention has a balance-sheet cost.

The deeper problem is not rainfall alone. The deeper problem is that India still runs a large economy with too much dependence on imported energy, imported edible oil, imported fertiliser inputs and rain-fed rural income.

This is why the prime minister’s consumption appeal was more important than it looked. The government was not simply asking people to save money. It was asking the household sector to become part of national external defence.

Gold purchases leak dollars. Foreign travel leaks dollars. Fuel consumption leaks dollars. Edible oil imports leak dollars. Fertiliser imports and gas-linked fertiliser costs leak fiscal and foreign-exchange space.

A bad monsoon worsens the same equation because it threatens domestic food supply and raises import sensitivity.

That is the real connection between Modi’s appeal, the rupee, oil, gold and El Niño.

Policy TestIndia’s first response should be blunt: protect food availability, but do not pretend buffer stocks are a water policy.

The real test is not whether India can survive one bad season. It can. The real test is whether India can reduce the number of citizens whose income still depends on a successful cloud system.

The policy map is clear.

India needs accelerated micro-irrigation, especially drip and sprinkler systems for vulnerable states and crops. It needs solar-powered irrigation where groundwater allows it and strict groundwater discipline where it does not. It needs crop planning that does not reward water-intensive choices in water-stressed regions. It needs edible oil security, better oilseed productivity and lower dependence on imported cooking oils. It needs fertiliser efficiency without suddenly shifting risk to farmers. It needs climate-resilient seed systems and crop insurance that actually pays when stress arrives.

Most of all, India needs the migration of labour from low-productivity agriculture into manufacturing and services to become faster, cleaner and more dignified.

A country cannot remain strategically comfortable when hundreds of millions of livelihoods still wait for the sky.

Market ReadingFor markets, the signal is equally clear.

A weak monsoon year is not merely an agri-input story. It is an FMCG volume story, a two-wheeler story, a tractor story, a cement story, a rural credit story, a power demand story, a fertiliser subsidy story, an edible oil import story and an RBI policy story.

If the monsoon weakens in the second half of the season, the first question will be food inflation. The second will be rural demand. The third will be policy room. The fourth will be the rupee.

The investor who treats monsoon as weather will miss the macro transmission.

The state that treats monsoon as an annual event will miss the structural warning.

The household that treats it as a distant farming issue will discover it in vegetable prices, fuel prices, milk prices and electricity bills.

🔴 Hidden Underpinning

India’s growth model still assumes that imported energy remains affordable and the monsoon remains broadly functional in the same year.

That assumption is now being tested.

A West Asia oil shock pressures the external account. El Niño pressures the food account. The rupee transmits both. Inflation converts both into politics.

This is why India’s next economic stress may not come from a bank, a stock-market crash or a budget number.

It may come from a chain that starts in Hormuz, travels through the Pacific, enters the monsoon, passes through the mandi, and arrives in the kitchen.

The monsoon is India’s second oil shock because it decides whether the imported-energy shock remains a fuel problem or becomes a food, inflation, rural-demand and currency problem.

That is the story now.

India is not only watching oil.

India is watching rain.

And in 2026, both may decide the same economy.

Source Basis

Reuters reports on Modi’s conservation appeal, India’s wholesale inflation, fuel-price hikes, monsoon risk and strong El Niño forecasts; NOAA Climate Prediction Center ENSO Diagnostic Discussion dated 14 May 2026; IRI mid-May 2026 ENSO forecast; Indian Institute of Tropical Meteorology historical all-India rainfall record; ICRIER Working Paper 276 on El Niño and Indian droughts; Drought Atlas of India 1901-2020; Economic Times report on foodgrain stocks; World Bank agriculture and employment indicators.